100% FREE LIVE IN PERSON PROPERTY MASTERCLASS

PROPERTY HACKING LIVE 2026!

How Singaporeans Are Generating an Extra $1,500–$4,000/Month From Property (Without Owning Multiple Homes)

If your property strategy still revolves around buy-and-hold residential, this exclusive session may challenge how you think about wealth building in Singapore.

You Did What Responsible People Do.

You studied hard.

Built a stable career.

Saved consistently.

Bought property.

Maybe you have also upgraded your home.

From the outside,

everything looks right.

But many Singaporeans eventually start asking...

“Is My Money Actually Working As Hard As I Am."

This is what I called:

The ❝Condo Trap❞

In Singapore, the most common property strategy is simple...

Buy A Private Residential Property, Hold It And Wait For It To Appreciate...

But today, the net yield of these properties sit around 2-3%.

Which means many Singaporeans like you and me have millions in property assets

But generates very Little Income from them.

The Real Issue Nobody Wants To Admit

Let's talk about what's actually happening here.

Imagine a $1.8M Condominium producing about $35K net income annually.

Now compare that with a typical household lifestyle cost of $120K - $150K per year.

You may need four or five similar properties to replace your income.

Under ABSD.

Under TDSR.

With rising prices.

For many Singaporeans, that timeline becomes very long.

The “Shift"

Instead of relying only on appreciation...

Savvy investors structure their property assets differently.

And this has helped increase the yield of the same property three folds without much effort on their part.

The same thing I did to grow our own property portfolio to 72 Million.

And It All Comes Down To These Three Core Principles

I Called “Wealth Pillars"

PILLAR #1

Controlling Bigger Assets

With Surprisingly

Little Capital.

In this Pillar, you'll discover how ordinary investors are quietly controlling commercial and industrial properties with surprisingly little money down while collecting rental income many assume only large investors can.

PILLAR #2

Turning An Average Property Into A High-Performing Income Asset

In this Pillar, you will discover a simple shift that can transform an average rental property into a much stronger income-producing assets. Most investors focus on buying the right property but experienced investor focus on this single thing.

PILLAR #3

Building Additional Income Without Having Huge Technical & Financial Knowledge

In this pillar, you will discover how ordinary Singaporeans are building additional income streams through property without needing complicated financial models or technical knowledge.

What You Are Going To Discover

(So you know this isn't one of those property seminars where they sell you property launches or just pure hype.)

#1 Why Traditional Buy-And-Hold Residential Property Isn't The Best Choice

For many years, buying and holding residential property was considered the safest path to wealth in Singapore.

But with yield that often averaging 2-3%, many Singaporeans today find themselves owning valuable property assets that generate a modest income.

We will also share insider information on where is the next growth area in Singapore and How you can make use of this golden window of opportunity.

#2 Our Property “ATM" System That Gives High Income Month On Month on Demand.

We will break down how different property structure, including commercial properties and structured co-living model can value add and exponentially change the income profile of an investment. You will discover how to create long term cashflow and sustainability for your properties.

You will also get our in-house playbook and checklist where you can refer to when finding your next investment properties.

#3 The Investor Playbook, How Savvy And Experienced Investor Evaluate And Find Golden Properties Opportunities

We'll walk through the key factors that we look at when it comes to analysing opportunities together during our closed door session.

This framework helps us think more strategically about how our property portfolio supports long term wealth building.

Meet Your Trainer

Jason Ng

CEO & Executive Chairman, Autagco Ltd

Today, Jason manages a portfolio of properties varies from commercial, industrial to conservation shophouses and food factories valued at over 72 Million.

Over the past 25 Years, he has helped more than 1000 individuals better understand how property can be used to build long term income and financial security through his Wealth Pillars Framework.

He also regularly share his views on property investing and financial education across media platforms like Channel 5, Channel 8, MoneyFM 89.3 and Capital 958.

He believes property investing should be structured, practical and accessible to everyday Singaporeans, not just large institutions.

(P.S. He enjoys singing in his free time)

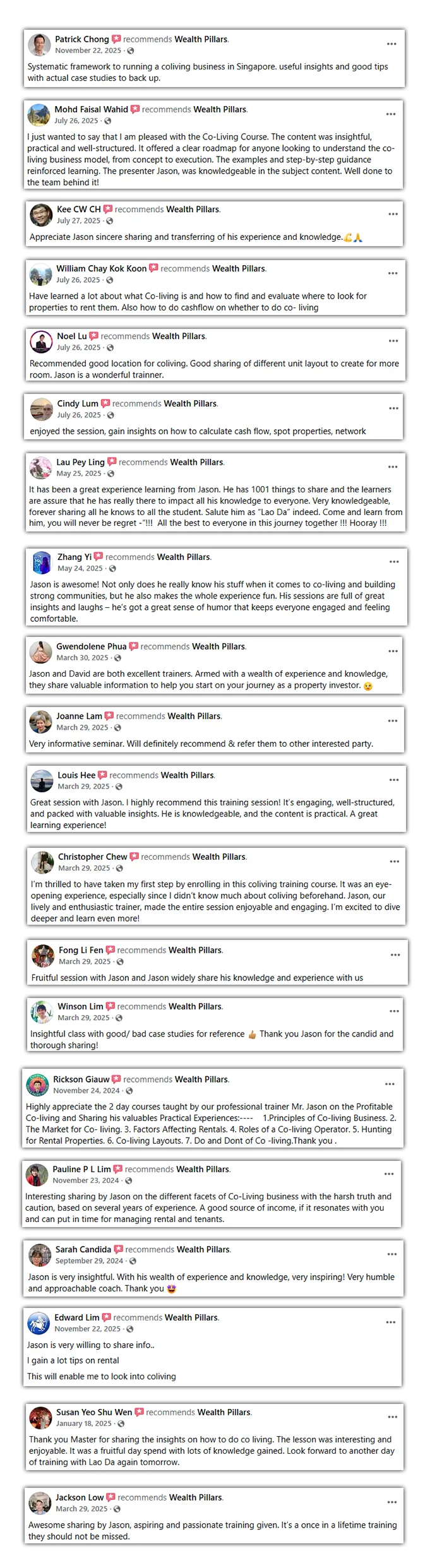

Here's What Past Attendees Have To Say About Us...

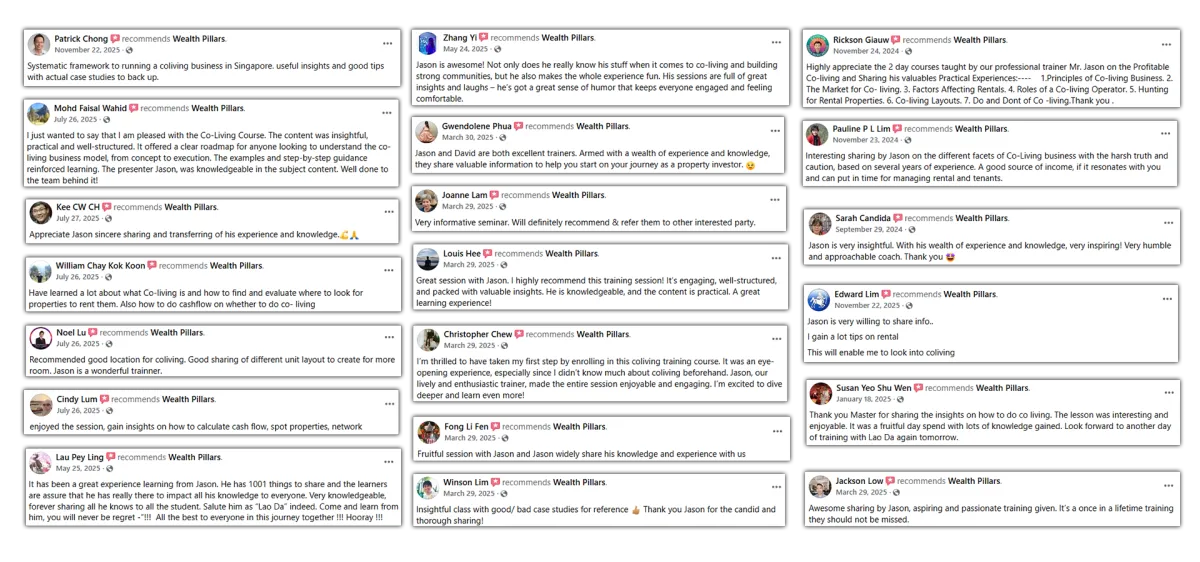

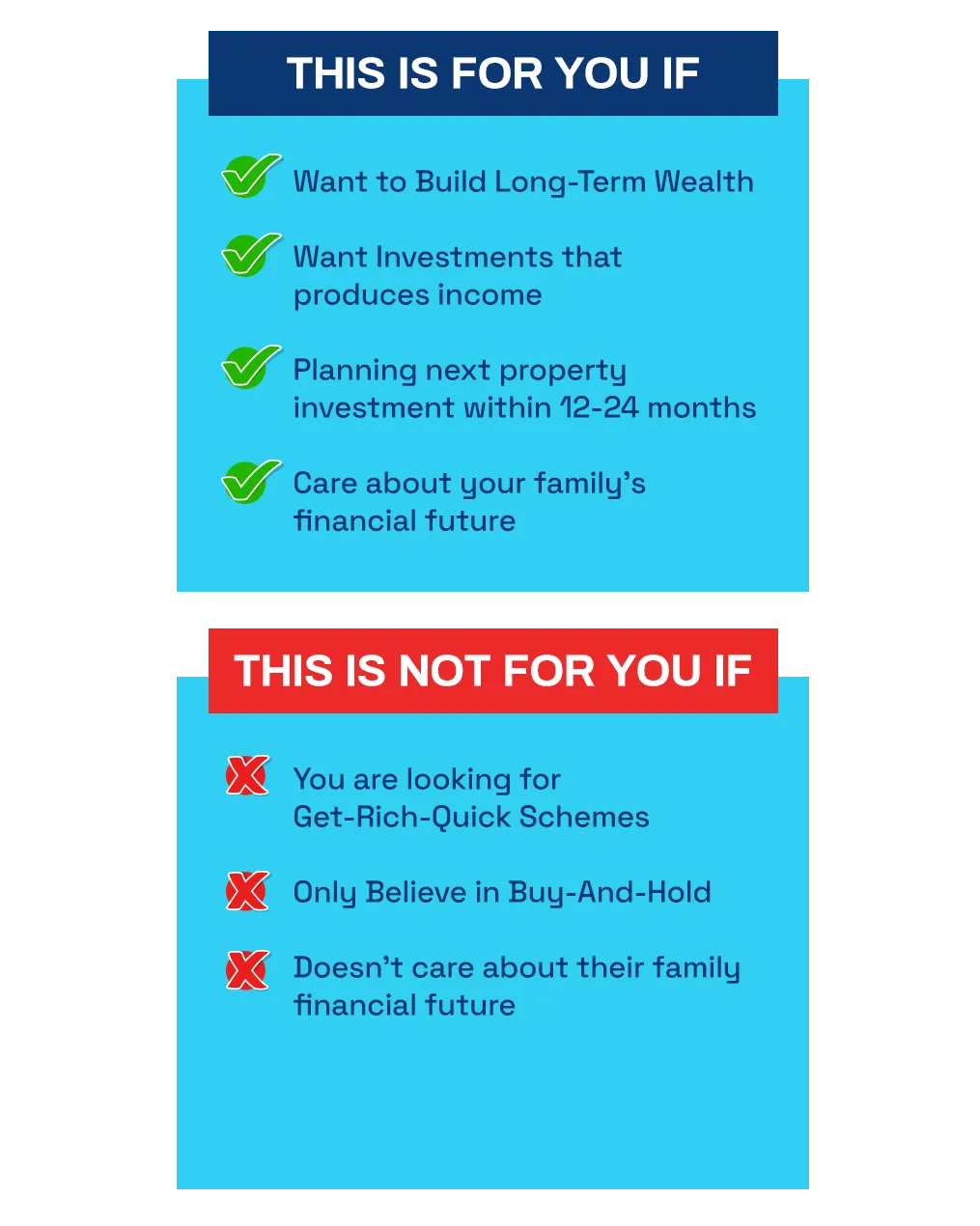

WHO THIS IS FOR

If you are still here...

One final thing...

Most people spend their lives focusing on earning income.

But financial security is often determined by how that income is invested.

Five years from now you will either say:

I'm glad I adjusted my strategy earlier.

Or

I wished I had looked into it sooner.

Only one decision moves you closer to financial freedom

Questions People Actually Ask

Is this a sales seminar or property launch.

No. This session is designed as a strategy session, not a developer sales presentation.

There will be no property launches or developer sales pitches. The focus of the session is to help participants understand different property investment structures and how they affect income and long-term wealth building.

Do I need property investing experience to attend?

Not necessarily.

Many attendees are professionals who already own a property and are considering their next investment move. The session focuses on helping participants understand how different property structures work, rather than assuming deep technical knowledge.

Is this session relevant to the Singapore property market?

Yes. The session specifically discusses property investing within Singapore’s regulatory environment, including factors such as ABSD, TDSR and local rental yield trends.

The goal is to help participants think about how property investments can be structured within Singapore’s unique market conditions.

Will specific property deals be shared during the session?

The session focuses primarily on investment frameworks and strategies, rather than promoting specific deals. The objective is to help participants understand how to evaluate property opportunities more strategically.

Who is this session most suitable for?

This session is generally most relevant for:

• professionals and business owners

• individuals planning their next property investment within 12–24 months

• those interested in building long-term income from property

Can I bring my spouse or partner?

Yes, and many attendees do.

Property decisions are often made as a family decision, so couples are welcome to attend together. (Do let us know if your partner has any dietary restrictions)

Will the session teach “get rich quick” strategies?

No.

The focus of this session is on long-term wealth building and income generation through property, not speculative or short-term investment tactics.

Is Lunch provided?

Yes. Lunch will be provided in a bento set. Our caterers are halal-certified however do let us know if you have any dietary restrictions (Non-Vegetarian or Vegetarian) when you are signing up.

Property Hacking Live is an educational event sharing general insights on property strategies. We do not guarantee financial results and individual outcomes will vary. Nothing presented should be considered financial, legal, or investment advice. This site is not affiliated with or endorsed by Facebook. Facebook is a trademark of Meta Platforms Inc.